As we move through 2026, many investors are focused on the year ahead. However, one of the most common questions I receive as a financial planner is whether it is "too late" to maximize tax-advantaged savings for the prior year.

The good news? It isn’t. You have until April 15, 2026, to make your IRA contributions for the 2025 tax year. This "grace period" is a rare opportunity to look back at your tax situation and shore up your retirement savings before the filing deadline.

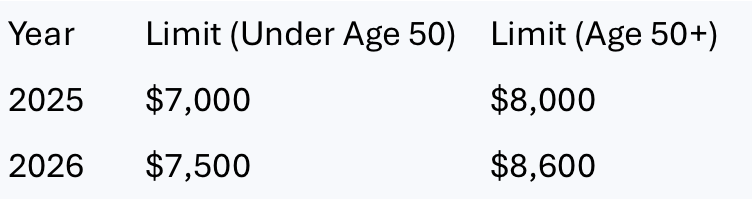

Below is a breakdown of the current landscape for IRA contributions and a guide on how to navigate the rules for 2025 and 2026.

2025 and 2026 Contribution Limits

The IRS recently increased the limits for 2026 to account for inflation. Whether you are contributing to a Traditional IRA or a Roth IRA, these are the maximum combined amounts you can put away:

Pro Tip: If you haven’t maxed out for 2025 yet, you can still contribute the full $7,000 (or $8,000) by April 15. Just be sure to specify "Prior Year Contribution" when making the transfer with your custodian.

What If You Don’t Have a 401(k)?

If you do not have access to an employer-sponsored retirement plan (like a 401(k) or 403(b)), the rules are actually in your favor regarding tax deductions.

- Full Deductibility: For those not covered by a workplace plan, your Traditional IRA contributions are fully tax-deductible, regardless of how much money you earn.

- The "Spousal" Rule: If you are married and you don't have a 401(k) but your spouse does, you can still get a full deduction as long as your joint income (MAGI) is below $236,000 (for 2025) or $242,000 (for 2026).

This is a significant advantage. While 401(k) participants often face "phase-outs" that prevent them from deducting IRA contributions if they earn too much, those without workplace plans can use the Traditional IRA as a powerful tool to lower their taxable income.

A Note for Married Couples Filing Separately

If you are married but choose to file your taxes separately, the IRS rules become quite restrictive. If you lived with your spouse at any time during the year:

- Your ability to deduct a Traditional IRA contribution phases out once your income exceeds $0.

- It is completely gone once you earn $10,000.

The same applies to Roth IRA eligibility. If you file separately, the window to contribute directly to a Roth is essentially closed if you earn more than $10,000. In these cases, we often look toward the "Backdoor" strategy.

The "Backdoor Roth" Strategy

If your income is too high to contribute to a Roth IRA directly ($165,000+ for singles or $246,000+ for joint filers in 2025), you can still get money into a Roth using this two-step maneuver.

How to do it:

- Contribute to a Traditional IRA: Open a Traditional IRA and make a non-deductible contribution (meaning you don't take a tax break for it).

- Convert to Roth: Once the funds have settled in the account (usually a few days), instruct your custodian to convert those funds into your Roth IRA.

- File Form 8606: When you file your taxes, you must include Form 8606 to show the IRS that you already paid taxes on that money so you aren't taxed again upon conversion.

WARNING: The "Pro-Rata Rule" Trap

This strategy works best if you have zero other Traditional IRA assets. If you have existing Rollover IRAs or SEP-IRAs, the "Pro-Rata Rule" applies, which could make the conversion partially taxable. Always consult with a professional before executing this.

Before you attempt a Backdoor Roth, you must understand the Pro-Rata Rule. This is the #1 reason these strategies go wrong.

The IRS does not see your IRAs as separate accounts; it views them as one giant bucket. If you have any pre-tax money in any Traditional, SEP, or SIMPLE IRA (such as an old Rollover IRA from a previous job), you cannot choose to convert only the new after-tax money. The IRS requires you to convert a proportional mix of pre-tax and after-tax dollars.

The Math in Action: Imagine you contribute $7,000 in after-tax money for a Backdoor Roth, but you already have a $93,000 Rollover IRA from an old 401(k).

- Total IRA Balance: $100,000

- After-Tax Portion: 7% ($7,000)

- Pre-Tax Portion: 93% ($93,000)

When you convert your $7,000 to a Roth, the IRS says only 7% ($490) is tax-free. The other $6,510 will be added to your taxable income for the year. This is often called the "Cream in the Coffee" rule—once you pour the cream (after-tax money) into the coffee (pre-tax money), you can’t just take a spoonful of only cream back out.

The Solution: If you have a large pre-tax IRA balance, we often recommend a "Reverse Rollover," where you move that pre-tax IRA money into your current employer’s 401(k). Since 401(k) balances are excluded from the pro-rata calculation, this "clears the deck" for a tax-free Backdoor Roth.

How We Can Help

Navigating these limits—and the tax implications of each move—is a core part of a comprehensive financial plan. At Harvest Financial Advisors, we are a fee-only, fiduciary firm. This means we are legally and ethically bound to act in your best interest, and we never receive commissions for product sales.

If you have a minimum of $500,000 in investable assets and are looking for a partner to help you with full financial planning, tax-efficient strategies, and retirement readiness, we would love to talk.

Ready to get your plan on track? Visit us at www.harvestadvisors.com or call our office today to schedule a consultation.

By: Monica Dwyer, CFP®, CDFA®, GFP